Potential Revenues for COVID-19

Print

Print Email

EmailIn order to assist our community members and partners, the Center for Local Government Finance and Policy has compiled brief overviews of COVID-19 response efforts as well as potential implications and impacts for local governments.

Potential Revenues for COVID-19

Summary

The outbreak of COVID-19 imposes great pressure on counties’ resources. From increased needs for health and social services to added law enforcement for stay at home order, counties along with other local government entities are working on the front line to keep their residents safe. Additional resources and revenues are needed more than ever to ensure critical services are delivered efficiently, effectively, and equitably. In this article we point counties to potential revenue sources, while noting capacity-building strategies to optimize these resources.

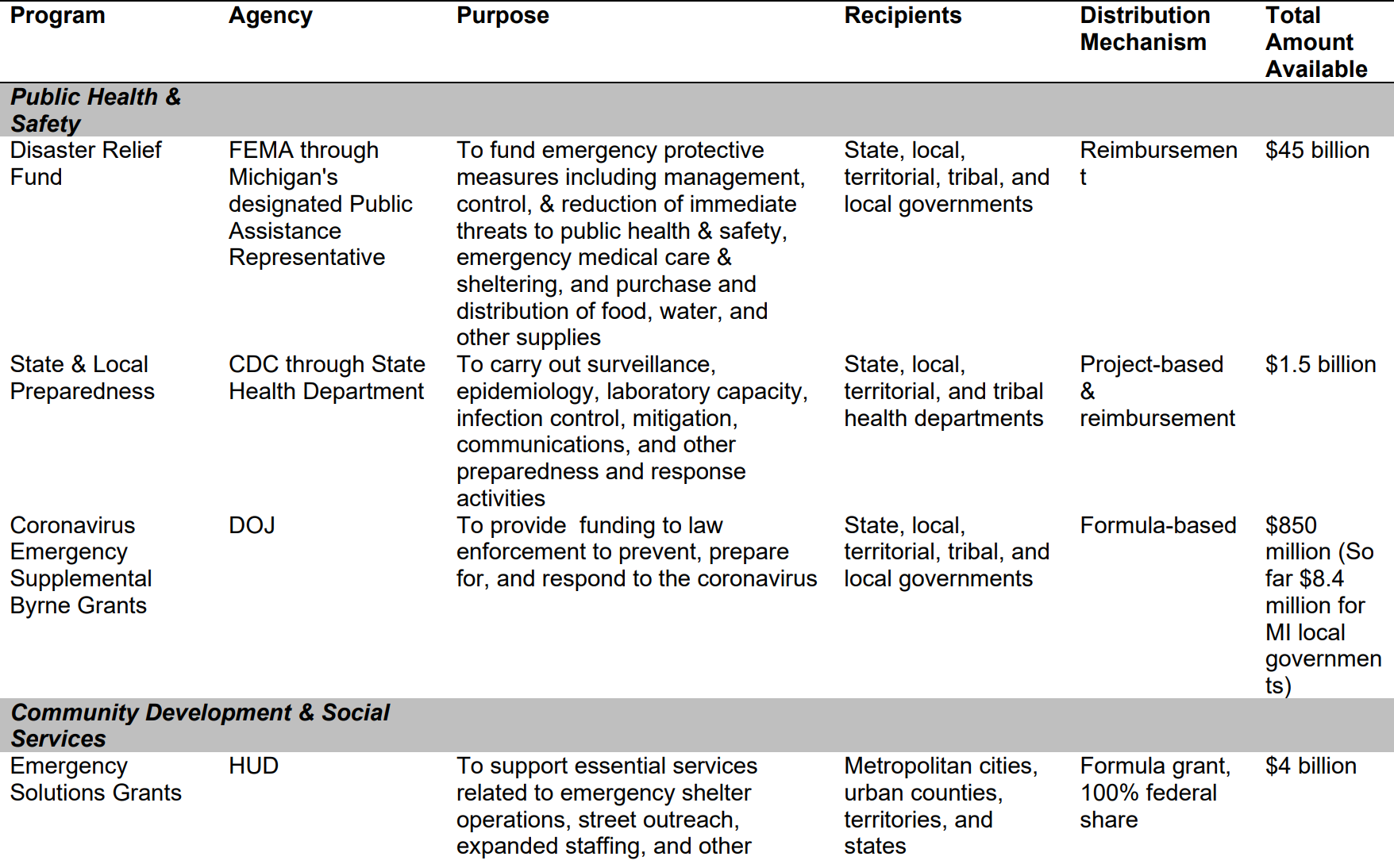

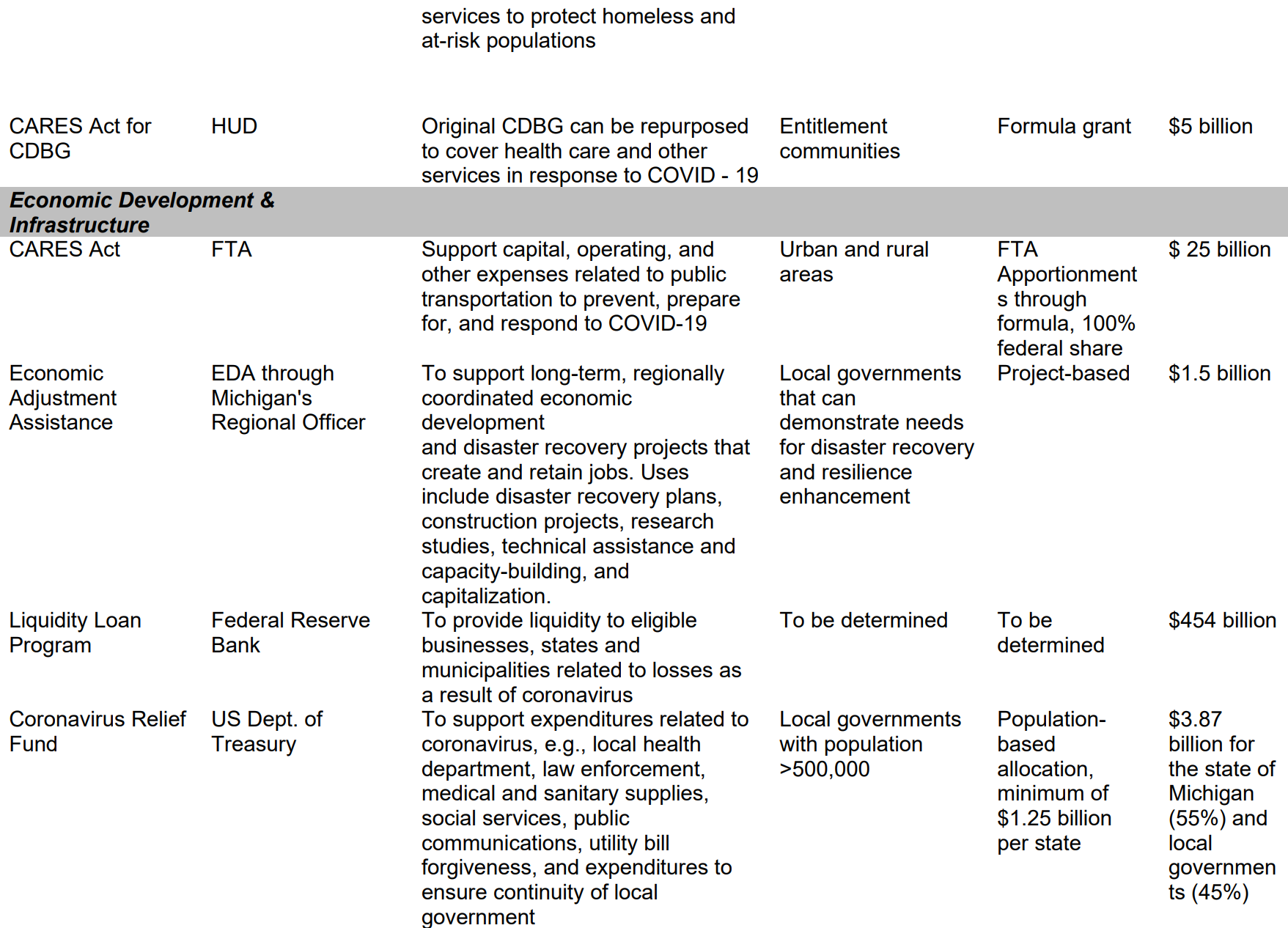

Federal Aid

Sweeping impacts of the pandemic require intervention at a larger scale. To this end, the federal government has provided support both through new appropriations like the Coronavirus Aid, Relief, and Economic Security (CARES) Act and through additional funding of existing federal programs. Organizations including International City/County Management Association (ICMA) and the MSUE Center for Local Government Finance and Policy at MSU have provided guides to understand and navigate the resources. Table 1 includes a list of federal grants and assistance made available to local communities to address various challenges due to COVID-19. Although not exhaustive, the list focuses on programs for which counties can be direct recipients and presents potential resources for various aspects of local operations.

Counties should also be mindful of the fact that some grants may be distributed to the state first and then administered by state designated officers. For instance, the Coronavirus Emergency Supplemental Funding Program by the Department of Justice has allocated $8 million to Michigan counties and municipalities, and according to the Michigan Association of Chiefs of Police, the following Michigan counties qualify for DOJ CESF program funds: Bay, Berrien, Calhoun, Eaton, Genesee, Grand Traverse, Ingham, Jackson, Kalamazoo, Kent, Macomb, Mecosta, Monroe, Muskegon, Oakland, Ottawa, Saginaw and St. Clair. This relief program provides support for coronavirus-related overtime, equipment including law enforcement and medical personal protective equipment, supplies such as gloves, masks, and sanitizer, hiring, training, and travel expenses particularly related to the distribution of resources to the most impacted areas. In this case, the efforts may be more productive with effective state-local communication and collaboration.

The federal government also reduces administration burdens for many of the grant applications. For example, HUD CDBG now has an expedited process to prepare or modify statement of activities. The HUD Secretary also has broader discretion for waivers to allow for flexibility for eligible uses. HUD Homeless Assistance Grants also eliminate planning and procurement requirements and habitability and environmental standards for temporary emergency shelters.

Property Taxes

In addition to addressing immediate needs for combating the pandemic, it is also crucial to plan ahead. At the federal level, there are discussions about multi-year stimulus package(s) for enhancing access to critical infrastructure such as drinking water, broadband, and transportation. Unfortunately, due to increased unemployment and business closures, counties have to prepare for the possibility that their own-source revenues, such as property taxes, would grow at a lower rate or even decline in the next couple of years. It would be helpful for counties to start identifying projects and services that anticipate increased spending in the near future, as well as explore revenue sources to support these functions. A couple options include:

Mills above the general limit. The state constitution sets a 15-mill cap on property taxes charged to any parcel in a given year, but also allows exceptions to the limit. Voters can raise this limit to 18 mills through referendum. Voters can also raise the limit to a total of 50 mills as long as the use of extra voted millage is specified, such as for parks, roads, water and sewer. On top of that, additional millage can be raised to repay general obligation debt whose issuance was approved by voters before. Mills above the general limit. The state constitution sets a 15-mill cap on property taxes charged to any parcel in a given year, but also allows exceptions to the limit. Voters can raise this limit to 18 mills through referendum. Voters can also raise the limit to a total of 50 mills as long as the use of extra voted millage is specified, such as for parks, roads, water and sewer. On top of that, additional millage can be raised to repay general obligation debt whose issuance was approved by voters before.

Special assessments. There has been increased use of special assessments in the past few years for public improvements. Historically, special assessments were used for capital projects, but gradually they were used to fund operations and services. Unlike general property taxes, special assessments are based on benefits that a community would receive due to the improvement. The special assessment rate is generally determined by the cost of a public improvement and the base on which the costs are to be apportioned. Unlike general property taxes, there is no limit on the special assessment rate.

Special assessments can provide designated revenues for public improvement projects and operations. Should a county anticipate increased needs for certain capital projects and local services, special assessments could be considered as a revenue tool. The use of special assessments may have legal, administrative, and political implications. Counties should be aware of their impacts on local communities before implementing special assessments.

Both options require stakeholder buy-in either through voter approval or property owner initiative. For special assessments imposed unilaterally by counties, voters can also oppose through petition referendum. Although the need for social distancing moves communication to a virtual platform and imposes challenges for stakeholder engagement, transparency and accountability are always critical. Communicating with residents about the need for additional revenues to sustain service delivery is important for garnering support and building trust.

Capacity Building

Apparently, it takes resources to get more resources. In order to maximize COVID-19 resources for your county, it is recommended for counties to establish a COVID-19 task force responsible for coordinating the County’s needs and resources. Members should understand the County’s structure and processes, implement strategies to identify and capture eligible and recoverable costs through funding sources, and identify and align priority projects and funding needs with available resources.

Counties are also encouraged to record and track the spending of county resources dedicated to COVID-19 response (county health departments/multi-county community health agencies, utilities, public safety, etc.) to demonstrate these expenditures were necessary and incurred due to the public health emergency. This tracking isolates to funding sources specific eligible and recoverable expenditures.

COVID-19 response (county health departments/multi-county community health agencies, utilities, public safety, etc.) to demonstrate these expenditures were necessary and incurred due to the public health emergency. This tracking isolates to funding sources specific eligible and recoverable expenditures.

Additionally, counties should track lost revenues (decline in property taxes, service fees, etc.) that are not directly accountable to COVID-19. This tracking will help Michigan counties communicate to Michigan’s congressional delegation their challenges and advocate for additional resources.

By: Shu Wang, Ph.D., Assistant Professor Mary Schulz, M.S., Associate Director MSUE Center for Local Government Finance and Policy