Bulletin E-3509

Bulletin E-3509 Insurance Options for Beef Growers

DOWNLOAD

January 7, 2026 - Jonathan LaPorte

Print

Print Email

EmailAs a decision-maker on a farm, you will need to manage many risks. Price and production risks are some of the most challenging risks to manage. Factors can include market prices, feed costs, or operating costs involved in raising livestock. Insurance for beef producers was created as a cost-effective means to aid farmers in managing or reducing the impact of these risks.

Livestock insurance is provided through the United States Department of Agriculture (USDA) Risk Management Agency (RMA). Insurance policies are managed by Approved Insurance Providers appointed by the USDA. They are privately owned companies that employ the policy underwriters, claims staff and agents necessary to carry out the insurance policies. They can be independently owned companies or part of agribusinesses that offer additional services.

Coverage policies are based on different types of income-based losses. Producers have the option to focus on price, gross margin, or revenue, depending on the policy. Each policy has its own set of criteria for eligibility and potential payouts.

Throughout this publication, we will review the basics of livestock insurance and present how its use can benefit your farm. This includes understanding the differences between policies, the ways each provides protection, and the advantages offered by each. We’ll also review how USDA RMA provides beginning farmers with additional benefits to assist in managing risks.

Livestock Risk Protection

During times of erratic cattle markets, price protection is an important management tool that producers can utilize to maintain farm profitability. RMA has implemented a market price insurance program since 2004. Cattle producers who take the opportunity to obtain market price protection often realize more income during times of falling cattle prices. Obtaining better pricing often requires developing marketing plans and market risk strategies.

Beef prices can also be severely impacted by events that occur in one day or overtime. In 2019, a fire at a large packing plant severely reduced harvest capabilities in the country. That single event drove prices of feeder cattle and market ready cattle down over the next several months. In 2020, many packing plants were shut down over various periods of time due to workers contracting COVID-19 and drove cattle prices lower. In both years, cattle producers sold both feeder cattle and market ready cattle at prices lower than expected.

Beef cattle producers have the opportunity to protect themselves from falling cattle prices by purchasing Livestock Risk Protection (LRP). The program allows producers to purchase market price protection insurance against falling markets. The insurance policy also fits with various size operations, giving both small and large producers an opportunity to obtain market price protection.

It is critically important to point out that LRP policies offer market price protection. It has no impact on the price producers receive from purchasers (feedlots, processors, etc.). Cattle are sold and marketed by producers in the method of their choosing. Consequently, producers are still encouraged to market cattle to the best of their ability. The actual LRP policy is only insurance against cattle market prices going lower. Note: Producers who raise Holstein steers and heifers can insure cattle with LRP but are only eligible to receive 50% of the futures value.

Feeder Cattle

Feeder Cattle contracts can be purchased for as few as one head and up to 12,000 head. Animals must be expected to weigh up to 1,000 pounds by the end of the insurance period. An annual limit of feeder cattle per producer in a year is 25,000 head. A year is considered July 1 through June 30.

Livestock eligible for coverage include calves, steers, heifers, predominately Brahman cattle or dairy cattle, and unborn calves. Unborn calves include beef and beef-on-dairy (Table 1). Coverage prices range from 75 to 100 percent of expected end value. Note: Coverage does not include the loss, death, or destruction of cattle.

Table 1: Feeder Cattle Classes and Weight Ranges Covered by Livestock Risk Protection (LRP)

|

Class |

Weight |

Covered Livestock |

|

Steers 1 |

0 – 5.99 cwt. |

Steers and bulls |

|

Steers 2 |

6.0 – 10.0 cwt. |

Steers only |

|

Heifers 1 |

0 – 5.99 cwt. |

|

|

Heifers 2 |

6.0 – 10.0 cwt. |

|

|

Brahman 1 |

0 – 5.99 cwt.. |

Heifers, steers, and bulls |

|

Brahman 2 |

6.0 – 10.0 cwt. |

Heifers and steers only |

|

Dairy 1 |

0 – 5.99 cwt. |

Heifers, steers, and bulls |

|

Dairy 2 |

6.0 – 10.0 cwt. |

Heifers and steers only |

|

Unborn Calves |

0 – 5.99 cwt. |

Note: Unborn calves are separated in individual classes for steers, heifers, brahman, and dairy. However, the weights are the same between classes. |

Fed Cattle

Contracts for Fed cattle can be purchased for as few as one head and up to 12,000 head. Animals must be expected to weigh between 10 cwt. (1,000 lbs.) to 16 cwt. (1,600 lbs.) by the end of the insurance period (Table 2). An annual limit of fed cattle per producer in a year is 25,000 head. A year is considered July 1 through June 30.

Table 2: Fed Cattle Classes and Weight Ranges Covered by Livestock Risk Protection (LRP)

|

Class |

Weight |

Covered Livestock |

|

Steers & Heifers |

10.0 – 16.0 cwt. |

Classes are further divided by individual month of coverage. |

|

Cull Cows |

10.0 – 16.0 cwt. |

Classes are further divided by individual month of coverage. |

Livestock eligible for coverage includes heifers, steers and dairy cull cows (Table 2). Coverage prices range from 75 to 100 percent of expected end value.

Importance of Policy Details

The Livestock Risk Protection program is for producers who want to watch cattle markets and pay attention to the details. Keeping a close eye on the market and details of your coverage is vital to maximizing potential benefits. Producers can sign a free application for LRP that does not bind them to any coverage. The application allows the producer the option to have the policy in place even the event they decide to place coverage.

LRP insurance is available for both fed cattle and feeder cattle at 13, 17, 21, 26, 30, 34, 39, 43, 47 and 52-week periods. Cull cows are limited to 13-week periods. Producers should try to purchase contracts with end dates as near as possible to actual cattle sale date. The period between contract end and cattle sale dates puts producers at risk that cattle markets can work against them.

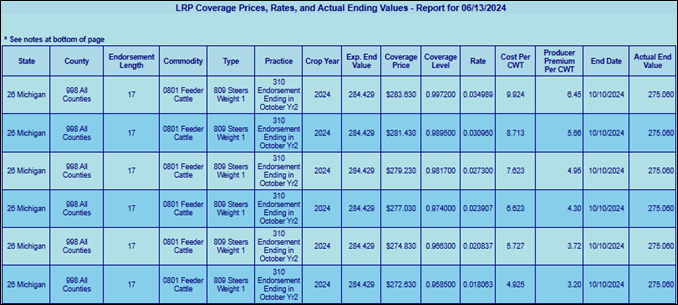

LRP works similarly to purchasing put options and setting a floor on the market price. The USDA-RMA publishes a state-specific daily report that is usually available around 4-4:30 p.m. Eastern Time and can be found at https://public.rma.usda.gov/livestockreports/main.aspx. That report indicates an expected ending value, various coverage levels, the cost per hundred weight of the policy and end date of the contract.

Figure 1. Example of LRP Livestock Report from USDA RMA dated June 13, 2024.

Producers need to ensure that insurance agents know they are getting ready to purchase insurance. Unlike crop insurance, RMA reports are published daily during the week in the late afternoon. Once producers decide to purchase insurance, the policy needs to be finalized by 9:25 AM Eastern Standard Time (EST) the following day.

Indemnity (Loss) Payment Calculation

At the end of the contract period, a loss adjuster will review the market and your contract to determine if an indemnity payment is due. An indemnity (loss) payment is made if the actual ending value is less than the coverage price. The payment considers the amount of livestock covered in the contract and their target weight. Coverage prices are also compared to actual ending value prices for the period. A producer’s share of the payment is considered when there are multiple parties insured under the contract.

[(Number of Covered Livestock x Target Weight) x (Coverage Price - Actual Ending Value)] x Insured Share

Table 3 provides an example scenario of indemnity payment. In the scenario, a producer took out a 17-week contract on June 13, 2024 (from Figure 1, line 2). The contract has 100 head of livestock with a target weight of 800 pounds (8.00 cwt). The contract uses a coverage level of 98.95% with a resulting coverage price of $281.43. An actual ending value was calculated using market reports from October 10, 2024, of $275.00. The producer’s share of the contract is 100%.

Table 3: Example of Indemnity (Loss) Payment for Livestock Risk Protection

|

Number of Covered Livestock |

100 head |

|

Target Weight |

8.00 cwt |

|

Number of Covered Livestock x Target Weight |

100 x 8.00 = 800 |

|

Coverage Price |

$281.43 per cwt |

|

Actual Ending Value |

$275.00 per cwt |

|

Coverage Price – Actual Ending Value |

$281.43 - $275.00 = $6.43 per cwt |

|

Indemnity (Loss) Payment |

800 x $6.43 = $5,144.00 |

The example in Table 3 outlines how producers utilizing LRP will have market price protection from decreasing cattle market prices. The example outlines that a loss payment of $6.43 per cwt ($281.43 - $275.00) was available to the producer due to lower market prices. Multiplied against the total 800 cwt for covered livestock (100 x 8.00) resulted in a payment of $5,144. Because the producer has 100% share of the contract, they also receive the entire indemnity payment.

Record Requirements

To be eligible for indemnity payment, you also have to provide documents that verify the sale of any livestock covered within the insurance period. Information must include:

- The seller’s name, which must match the insured name in the policy.

- The purchaser of livestock.

- The date of sale.

- The number of livestock sold.

- The average weight of the livestock sold.

Note: average weight is not required for unborn livestock. However, documents that verify proof of ownership interest in the animals that any covered livestock were born from are required.

In some cases, additional records may also be required. Visit RMA’s Livestock Insurance Plan website for more information: https://www.rma.usda.gov/policy-procedure/general-policies/livestock-insurance-plans-resources

Livestock Gross Margin

The Livestock Gross Margin program (LGM) focuses on both livestock prices and feed costs. It provides risk protection against falling livestock prices and rising feed costs, or both. However, it does not insure against cattle death, unexpected increases in feed use, or even anticipated or multiple year increases in feed use.

A simple formula is used to calculate the gross margin covered under the program. Gross margin equals the market value of the livestock minus feed costs.

Futures prices are used to determine market prices. Prices are based on simple averages of futures contract daily settlement prices. Similar to LRP, there is no influence from LGM on the prices actually received by producers. Cattle are sold and marketed by producers in the method of their choosing.

Feed costs are determined by using a fixed amount of corn bushels. Bushels are priced using commodity futures prices for corn. The corn bushels used in the calculation depend on the type of endorsements used within the program. LGM can be purchased for cattle using two different types of endorsements:

- Finishing Yearlings – Intended for 750-pound feeder cattle to be finished to 1250 pounds and uses a fixed corn amount of 50 bushels.

- Finishing Calves – Intended for 550-pound feeder cattle to be finished to 1150 pounds and uses a fixed corn amount of 52 bushels.

The insurance period is an important consideration for setting contracts. Cattle producers are covered for an 11-month period after the policy deadline, or sales closing date. For example, an insurance period for a sales closing date in January would include February through December. However, coverage begins the second month of the insurance period. In this example coverage would be March through December. Each month of the insurance period must include the target number of cattle you elect to insure (also known as target marketings).

Another important component of the Livestock Gross Margin program is selecting a deductible. A deductible is the portion of the expected gross margin that you choose not to insure. Deductible amounts range from $0 to $150 per head, in $10 increments. The deductible is calculated by multiplying the selected head deductible by the total target number of cattle sold (total target marketings) across all months in the insurance period.

Indemnity (Loss) Payment Calculation

At the end of the contract period, a loss adjuster will review the market and your contract to determine if an indemnity payment is due. To receive an indemnity payment, the actual gross margin must be less than the gross margin guarantee for the insurance period.

Futures prices and feed costs are used to calculate an expected gross margin or the anticipated difference between the market value of livestock and the cost of inputs (feeder cattle and feed). Consider the formula used for finishing yearlings, which are 750-pound feeder cattle that will be finished at 1,250 pounds. Note: pounds are converted to cwt for the formula below:

(12.5 cwt. x Live Cattle Price) – (7.5 cwt. x Feeder Cattle Price) – (50 Bushels x Corn Futures Price)

After calculating the expected gross margin, the next step is to identify the gross margin guarantee. The gross margin guarantee is the expected total gross margin for an insurance period minus the deductible times the total of target marketings.

Gross Margin Guarantee = (Expected Gross Margin – Deductible) x Total Target Marketings

RMA supplies a listing of expected gross margins each month for both endorsements. Note: expected and actual gross margins, once calculated, are available by accessing RMA’s Actuarial Information at: https://www.rma.usda.gov/tools-reports/actuarial-documents.

An example of the Gross Margin Guarantee calculation is provided below (Table 4). For a January contract with an effective date of June 12, 2025, RMA lists the expected gross margin for finishing yearlings in Michigan as $4.41 per cwt or $441 per head. Subtracting a deductible of $10 per head on a 100 head contract, the gross margin guarantee would be calculated as $4.31 per cwt or $431 per head.

Table 4: Example of Gross Margin Guarantee Calculation for Livestock Gross Margin

|

Expected Gross Margin |

$441 per head |

|

Deductible |

$10 per head |

|

Target Marketings |

100 |

|

Gross Margin Guarantee |

($441 - $10) x 100 = $43,100 |

The final step of calculating an indemnity payment is to compare the gross margin guarantee against the actual gross margin. The indemnity payment is calculated as:

Gross Margin Guarantee – Actual Gross Margin = Indemnity Payment (if positive)

Table 5: Example of Indemnity Payment Calculation for Livestock Gross Margin

|

Gross Margin Guarantee |

$431 per head |

|

Actual Gross Margin |

$413 per head |

|

Total Target Marketings |

100 head |

|

Indemnity Payment |

($431 - $413) x 100 = $1,800 |

Consider in Table 5 if the actual gross margin was priced at $4.13 per cwt or $413 per head. As Table 5 outlines, because the actual gross margin was less ($413) than the gross margin guarantee ($431), the indemnity payment rate is $18 per head ($431 - $413). Multiplied by the 100 head of total target marketings, this results in an indemnity payment of $1,800.

The example contract illustrates the benefits of using the Livestock Gross Margin when risk concerns regarding both price and costs are involved. Of course, when producers are evaluating risk, the cost of the premium must be considered.

Record Requirements

The record requirements for Livestock Gross Margin policies are different from some other policies.

The main difference is that you don’t have to provide records up front, but you must retain them for a minimum of three years. USDA may request to examine them or require that they be produced during the retention period. Records include documentation relating to breeding, feeding, finishing, and sale of cattle. Requests for records can include purchase, feeding, shipment, sale, or other disposition of all insured livestock. USDA also reserves the right to examine the insured cattle during the insurance period.

For more information on record requirements related to cattle, review the policy documents at: https://www.rma.usda.gov/policy-procedure/general-policies/livestock-insurance-plans-resources

Premiums & Subsidies

Livestock insurance is not free and requires a premium to be paid for its use. The premium for each type of policy will increase or decrease based on the coverage level you elect.

For example, recall Figure 1 with the report for 17-week-long Livestock Risk Protection contracts. Line two at a coverage level of 98.95% shows that a premium of $5.66 per cwt is paid. Compared to a higher coverage level of 99.72% (line one) with a premium of $6.45 per cwt and a lower coverage level of 98.17% (line three) with a premium of $4.95 per cwt.

Despite the costs associated with insurance, know that premiums are highly subsidized by the USDA. Therefore, the premium you pay is not the full price for the insurance. These subsidies increase or decrease based on the coverage level you elect as well. Table 6 highlights subsidies associated with Livestock Risk Protection:

Table 6. Subsidy Factors for Feeder Cattle under Livestock Risk Protection

|

Coverage Level |

70% - 79.99% |

80% - 84.99% |

85% - 89.99% |

90%- 94.99% |

95% - 100% |

|

Subsidy |

55% |

50% |

45% |

40% |

35% |

For Livestock Gross Margin, subsidies are based on the deductible selected for the contract. The higher the deductible being paid, the higher the subsidy applied to the final premium costs. Note: Producers can select or target individual months for coverage. However, to obtain the full subsidy through LGM, coverage must be placed in two calendar months.

For example, if a $0 deductible is chosen, then a subsidy of 18% is received. For a $10 deductible, the subsidy level is 20%; for a $20 deductible, the subsidy level is 23%. However, if the highest deductible at $150 is chosen, then a subsidy of 50% is received on the premium.

Note: For both LRP and LGM policies, the premium is not due until two months after the selected coverage ends.

Additional Subsidy Support for Beginning Farmers

Beginning farmers receive an additional 10 percentage points of premium subsidy toward existing coverage policy. The percentage points increase the subsidy and reduce the overall premium for the insurance. This applies to all insurance policies that have a subsidized premium through the USDA RMA. USDA RMA defines a beginning farmer as “an individual who has not actively operated and managed a farm or ranch with an insurable interest in a crop or livestock as an owner-operator, landlord, tenant, or sharecropper for more than 10 crop years." For more information visit: https://www.rma.usda.gov/about-crop-insurance/frequently-asked-questions/beginning-farmer-rancher-bfr-veteran-farmer-rancher.

Whole-Farm Revenue Protection

An additional option that can be used on its own or combined with individual insurance policies is a Whole-Farm Revenue Protection (WFRP) plan. It provides coverage for all commodities on a farm under one insurance policy. Designed for farms with up to $17 million in insurable revenue, it covers both crops and livestock. A WFRP plan also covers revenues for farms that are marketed to local, regional, farm-identity preserved, specialty, or direct markets. However, no more than 50% of total revenue from commodities must be purchased for resale.

Record Requirements

You must provide certain documents to ensure eligibility for WFRP insurance. These records include:

- Five consecutive years of Schedule F or other farm tax forms.

- Supporting information verifying tax forms are accurately filed with the Internal Revenue Service may be needed.

- If applicable, information supporting your farm as an expanding operation due to physical expansion last year or in an upcoming year. Expansion activities include increased acres, added equipment such as a greenhouse, new varieties or planting patterns, or anything that expands production capacity beyond price changes.

Exceptions to record requirements include:

- Beginning or veteran farmers may qualify with three consecutive years of Schedule F or other tax forms if farmed in previous year. If you qualified as a beginning farmer or veteran farmer in the previous year, four years of tax forms are needed.

- Physical inability to farm for one out of five required historic years may qualify if farming in previous year.

- You operate as a tax-exempt entity (such as a Tribal entity) and have third-party records available to complete substitute Schedule F tax forms to demonstrate a five-year history.

Calculating the Revenue Guarantee

Farm records are an important part of determining your farm’s approved revenue. An approved revenue is used to determine your amount of insurable revenue based on your historic gross income. The historic gross income is averaged over five years, as reported on Schedule F income tax forms. As of 2020, new provisions reduce impacts on gross income due to losses during your five-year history. For example, a revenue exclusion excludes the lowest year, and the remaining four years are then averaged into an adjusted historic average revenue. The adjusted historic average revenue is compared to expected revenues for an upcoming crop year. Whichever of these two revenue numbers is lower, it becomes the approved revenue. Another option is a revenue substitution that replaces a poor revenue year with 60% of your simple average allowable revenue based on your five-year history. A final option is a revenue cup, which establishes that revenue cannot fall below 90% of the previous year’s approved revenue.

Note: Expected revenues must be based on allowed revenue streams. Examples of nonallowable revenue streams include custom-hired agricultural work, contract growing, government program payments (such as Conservation Reserve Program participation), and post-production processing.

The insured revenue is calculated by multiplying your approved revenue by your coverage level:

Approved Revenue x Coverage Level (%) = Insured Revenue

Coverage levels range from 50% to 85%, similar to other insurance policies (see Table 7). Revenue coverage amounts are limited to a maximum of $17 million. Coverage of revenue from greenhouses or nurseries is limited to $2 million, with an exception noted for aquaculture related commodities.

Table 7: Maximum Farm Approved Revenue at Each Coverage Level

|

Coverage level |

Commodity count (Minimum required) |

Maximum farm approved revenue (MFAR) |

Maximum insurable revenue |

|

85 |

1 |

$20,000,000 |

$17 million |

|

80 |

1 |

$21,250,000 |

$17 million |

|

75 |

1 |

$22,666,667 |

$17 million |

|

70 |

1 |

$24,285,814 |

$17 million |

|

65 |

1 |

$26,153,846 |

$17 million |

|

60 |

1 |

$28,333,333 |

$17 million |

|

55 |

1 |

$30,909,091 |

$17 million |

|

50 |

1 |

$34,000,000 |

$17 million |

Farms with two or more commodities automatically receive a whole-farm subsidy, while farms with only one commodity receive an enterprise subsidy.

Indemnity (Loss) Payment Calculation

At the end of the season, after you have filed your farm income taxes, a loss adjuster will review your records. The adjuster will look for allowable revenue and expenses, inventory adjustments, unharvested or unsold production, and production lost from causes not covered by the program. The adjuster will use your farm records to determine an actual total farm revenue. A loss indemnity payment is made when your farm’s actual total revenue falls below the insured revenue.

Revenue Guarantee – Actual Revenue = Indemnity Payment (if positive)

Micro Farm Program

A Micro Farm Program (MFP) is similar to a WFRP plan. It also provides coverage for all commodities on a farm under one insurance policy, including both crops and livestock. No more than 50% of total revenue from commodities must be purchased for resale. An MFP also covers revenues for farms that market to local, regional, farm-identity preserved, specialty, or direct markets. Farmers can drop their lowest year out of five for purposes of revenue calculation.

A key difference for an MFP policy is that it is designed for farms with up to $350,000 in insurable revenue. The insurable revenue increases to $400,000 if you held a policy in the previous year.

Additional Differences from Whole-Farm Revenue Protection

Additional differences exist with an MFP compared to a WFRP policy. Those differences include:

- A minimum of only three consecutive years of Schedule F or farm tax forms are needed to determine an approved revenue, including the most current year.

- Beginning or veteran farmers/ranchers can use another person’s tax records when purchasing or inheriting a farm operation if they have materially participated in the operation or management of that farm.

- If your farm has been expanding over time, approved revenue may be allowed to increase. Five years of consecutive years of revenue history and measurements of growth are needed to verify expansion.

- A WFRP policy uses individual prices to value commodities. In an MFP policy, one value for all commodities will be calculated for your farm, based on average revenues from your farm history.

- Value-added products are insurable revenue for MFP, unlike in WFRP where they are excluded.

Indemnity (Loss) Payment Calculation

Indemnity payments are also handled similarly to a WFRP policy. At the end of a season, a loss adjuster will review your records. The adjuster will use your farm records to determine an actual total farm revenue. A loss indemnity payment is made when your farm’s actual total revenue falls below the insured revenue.

Revenue Guarantee – Actual Revenue = Indemnity Payment (if positive)

Final Thoughts & Recommendations

In addition to the policy options outlined in this publication, there are also private nonsubsidized (peril) policies on the market. The cost vs. benefit of these policies varies widely, but an insurance agent can help guide the decision of what is best for each individual farm.

Producers can purchase market protection from insurance agents in a similar manner to buying crop insurance. Agents selling crop insurance frequently sell livestock policies.

Michigan State University Extension recommends visiting with an insurance agent to discuss the policy options and risk scenarios that exist for your farm operation. Due to the number of details and options within insurance policies, deciding what to do can become complicated. A strong working relationship with your agent can be helpful when it comes to record keeping, program analysis, and program rollout notifications. Agents can provide specific details on eligibility, timelines, and documentation requirements for policies and options of interest.

To visit with a crop insurance agent, use the Agent Locator Page offered through the USDA’s RMA (https://www.rma.usda.gov/tools-reports/agent-locator).