Are you creditworthy?

Print

Print Email

EmailCredit scores, credit reports and the five C’s can all affect your creditworthiness.

What is creditworthiness?

In the simplest definition by Merriam Webster’s dictionary, creditworthinessis your ability to repay borrowed money. Knowing your creditworthiness is important because it can affect your ability to get a loan, car, job, housing, insurance and more.

How do you know if you are creditworthy?

The higher your credit score indicates you have greater creditworthiness. FICO credit scores range from 300-850. Any score above 800 is considered excellent. According to Experian, one of the three national credit reporting agencies, the average American FICO credit score was 703 in 2019, which is considered good.

To make sure your credit score is accurate, you can check your credit history by requesting a credit report. Michigan State University Extension suggests to make it a habit to check your credit report on a regular basis. In fact, through April 2021, everyone in the U.S. can get a free credit report each week from all three national credit reporting agencies (Equifax, Experian, and TransUnion) at AnnualCreditReport.com.

How do lenders determine your creditworthiness?

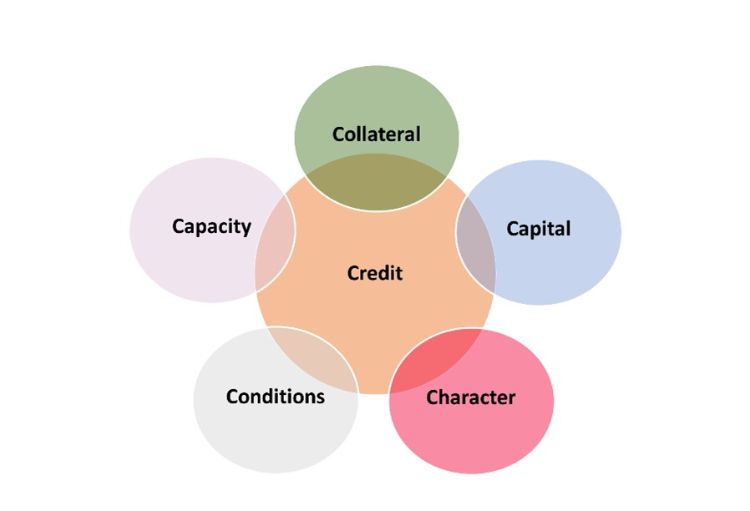

Lenders look at many factors to decide whether a loan will be granted and under what terms. They will request a copy of your credit report and review the five C’s—capital, collateral, character, capacity and conditions—to help determine the risk of lending. Each is described briefly below.

- Capital is a term for financial assets an individual or business has such as cash, liquid assets or Lenders appreciate when a borrower can cover some of the loan costs with existing wealth. Having the ability to make a down payment or pay for closing costs on a home may give the lender confidence that you can manage your funds to repay on time.

- Capacity refers to the borrower’s ability to repay what was loaned based on current income and debt. No one wants to loan money to someone who has no way to pay it back. Lenders want to make sure you have more money coming in than going out. A history of steady employment and increasing income makes them feel more confident about lending to you.

- Character refers to the borrower’s integrity and reputation. As history is the best predictor of the future, lenders request credit reports on applicants to see how they have used credit in the past. For business loans, lenders may also look at the applicant’s background, education, industry knowledge and experience required to successfully operate the business.

- Collateral refers to something of value used to secure a loan such as a house, car or money in a savings account. If the borrower defaults on the loan, the lender can seize the collateral as partial payment. Having collateral reduces a lender’s risk making a loan more attractive.

- The conditions of the loan, such as its interest rate and amount of money put down towards the principal (the money you borrow) influence the lender's desire to finance the borrower. Conditions can also refer to how a borrower intends to use the money. Consider a borrower who applies for a car loan or a home improvement loan. A lender may be more likely to approve those loans because of their specific purpose, rather than a signature loan, which could be used for anything. Additionally, lenders may consider conditions that are outside of the borrower's control, such as the state of the economy, industry trends or pending legislative changes.

Michigan State University Extension and Michigan 4-H Youth Development have programs and resources to empower adults and youth to make healthy financial decisions. For more information on career exploration, workforce preparation, financial education, or entrepreneurship, contact 4-HCareerPrep@msu.edu.