Premiums for beef-dairy cross calves shrinking in percentage terms

Print

Print Email

EmailWhile premiums for beef-dairy cross calves versus dairy bull calves have increased in dollar terms over the past six years, they have decreased in percentage terms.

In the United States, breeding dairy cows with beef semen was not considered common practice prior to 2017. However, the units of beef semen sold in the U.S. increased 283% from 2.54 million in 2017 to 9.73 million in 2024. Meanwhile, domestic dairy semen sales have decreased by 7.01 million units during the same period. These domestic semen sales numbers reflect the adopted practice of beef-on-dairy crossbreeding by dairy producers in the U.S. A combination of factors such as low milk prices, increased use of female sexed semen, and low prices for male and female dairy calves prompted the adoption of beef × dairy crossbreeding for greater monetary returns for dairy operations.

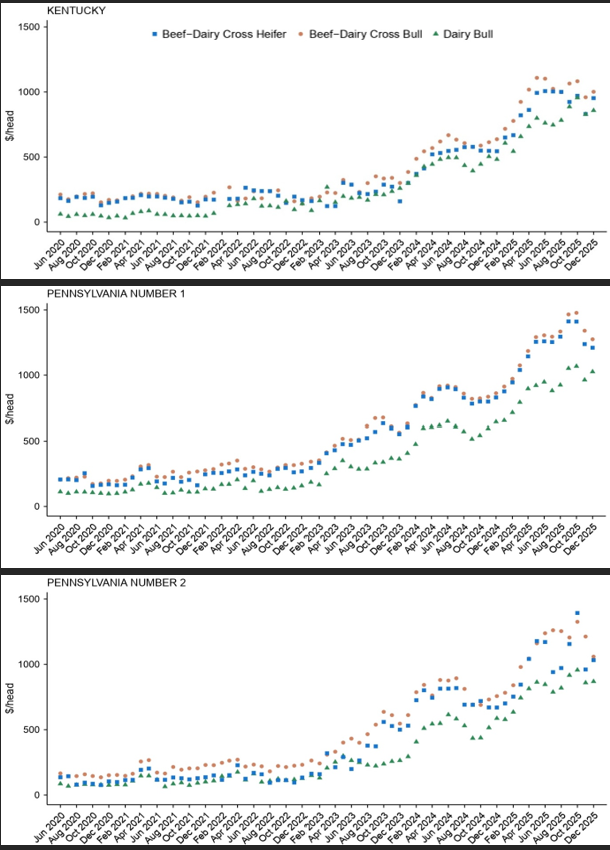

Data from three recurring USDA Agricultural Marketing Service reports were used to determine price differences between 1) dairy bull calves and beef-dairy cross bull calves, 2) dairy bull calves and beef-dairy cross heifer calves, and 3) beef-dairy cross bull calves and beef-dairy cross heifer calves. These data come from the Farmers Regional Livestock Glasgow Dairy Auction in Smiths Grove, KY; the Monday New Holland Livestock Cattle Auction in New Holland, PA; and the Thursday New Holland Livestock Cattle Auction in New Holland, PA.

Spanning mid-2020 through 2025, 67 months of quantity-weighted average prices were amassed for dairy bull, beef-dairy cross bull, and beef-dairy cross heifer calves for the Kentucky and Pennsylvania sales. For the Pennsylvania sale, calf prices are further broken down into Number 1 and Number 2 grades as defined by the U.S. Grade Standards for Feeder Cattle. Figure 1 plots monthly quantity-weighted prices for each of the three-price series across the three sales.

As shown in Figure 1, Kentucky, Pennsylvania Number 1, and Pennsylvania Number 2 sales each see sharp increases in calf prices over time. Several factors are likely contributing. First, the U.S. beef cow inventory is at its lowest level since the early 1960s, driven by market dynamics, drought impacts, and biological lags. Concurrently, consumer demand for beef remains robust. Hence, calves entering the beef supply chain are a hot commodity.

Table 1 summarizes differences between quantity-weighted average beef-dairy cross bull calf and dairy bull calf prices by year in both dollar and percentage terms. Across the Kentucky, Pennsylvania Number 1, and Pennsylvania Number 2 sales, $/head price differences between beef-dairy cross bull and dairy bulls have generally increased from 2020 through 2025. For example, beef-dairy cross premiums compared with dairy increased for Pennsylvania Number 1 bulls from $96.78/head in 2020 to $341.32/head in 2025. That said, percentage premiums for Pennsylvania Number 1 beef-dairy cross bulls versus dairy bulls decreased from 91% in 2020 to 38% in 2025. For Kentucky and Pennsylvania Number 2 sales, the 2025 percentage premiums were 29% and 38%, respectively.

Table 1. Mean differences between quantity-weighted average beef-dairy cross bull and dairy bull calf price by sale, grade and year

|

YEAR |

KENTUCKY |

PENNSYLVANIA Number 1 |

PENNSYLVANIA Number 2 |

|||

|

|

$/head |

% |

$/head |

% |

$/head |

% |

|

2020 |

141.37 |

282 |

96.78 |

91 |

71.64 |

92 |

|

2021 |

135.22 |

250 |

123.85 |

99 |

98.48 |

102 |

|

2022 |

70.36 |

56 |

154.60 |

103 |

101.00 |

80 |

|

2023 |

80.38 |

43 |

226.55 |

78 |

201.18 |

83 |

|

2024 |

138.93 |

32 |

266.56 |

47 |

277.51 |

57 |

|

2025 |

218.28 |

29 |

341.32 |

38 |

306.35 |

38 |

Table 2 reveals similar findings for beef-dairy cross heifer and dairy bull calf prices. Again, taking the Pennsylvania Number 1 sale for example, we find the premium for the beef-dairy cross calves was $88.92/head in 2020 but rose to $291.89/head in 2025. However, percentage differences fell from 82% in 2020 to just 32% in 2025. The percentage premiums for beef-dairy cross heifers versus dairy bulls in 2025 were 17% and 24%, for Kentucky and Pennsylvania Number 2 auctions, respectively.

Table 2. Mean differences between quantity-weighted average beef-dairy cross heifer and dairy bull calf price by sale, grade and year

|

YEAR |

KENTUCKY |

PENNSYLVANIA: Number 1 |

PENNSYLVANIA: Number 2 |

|||

|

|

$/head |

% |

$/head |

% |

$/head |

% |

|

2020 |

120.14 |

239 |

88.92 |

82 |

25.06 |

29 |

|

2021 |

119.07 |

220 |

83.00 |

65 |

34.76 |

36 |

|

2022 |

74.40 |

60 |

111.47 |

75 |

9.19 |

5 |

|

2023 |

22.71 |

10 |

189.01 |

65 |

98.63 |

34 |

|

2024 |

64.39 |

14 |

242.97 |

43 |

223.72 |

46 |

|

2025 |

126.87 |

17 |

291.89 |

32 |

204.60 |

24 |

The contrast between the trends in dollar and percentage terms summarized in the previous tables stems from increasing prices across the board. Simply put, the prices garnered for all animals entering the beef supply chain are greater today than they were at the beginning of the decade. Consequently, the price differences between beef-dairy cross calves and dairy bulls have been growing in dollar terms while simultaneously decreasing in percentage terms. For further analysis, price differences between beef-dairy cross bull calves and beef-dairy cross heifer calves are explored in the paper linked at the end of this article.

The greater price paid for beef-dairy cross bull and heifer calves relative to dairy bull calves is consistent with the expectation of higher value further down the beef supply chain. This greater value for beef-dairy cross calves could be captured by greater average daily gain and fewer days on feed during the preweaning and postweaning calf grower stage prior to feedlot entry. Additionally, beef-dairy cross calves may achieve better carcass grades and associated yield and quality premiums from processors.

Broader market trends likewise impact the price of beef-dairy cross calves. Low U.S. beef cow inventory numbers mean fewer beef calves entering the beef supply chain. In turn, demand for beef-dairy cross calves has increased to fill that supply gap, meaning calves produced from dairy operations, including beef-dairy cross calves, are making up a greater proportion of the fed cattle supply. This strong demand for beef-dairy cross calves will likely fluctuate as the cattle cycle changes supply fundamentals. When beef cow inventory numbers increase, beef-dairy cross calves could be positioned to take a larger relative drop in prices as compared to beef calves because buyers will have the ability to be more selective in the animals they purchase. Data from future market sale reports, along with beef-dairy cross and dairy bull calf rearing economic data, will determine if the explored trends in price differentials will continue for years to come.

Details of the full study are featured in the article “Market price differences between beef-dairy cross calves and dairy bull calves from Kentucky and Pennsylvania auctions” published in Applied Animal Science.